JVL Wealth Strategies moves office, positions for future growth

December 13, 2021

JVL Wealth Strategies hires wealth manager

March 9, 20222021 YEAR END REVIEW

US MARKETS

INTERNATIONAL MARKETS

S&P 500

Looking back over the last 22 years, the S&P 500 price only Index (excluding dividends) has experienced three bear markets, yet has gained 224% from where it began on January 1, 2000.

The S&P 500 total return (including dividends) was another positive year. Looking over a longer time period we see that the S&P 500 has been positive in 71 of the past 96 years meaning that 74% of those years (1926 – 2021) have shown positive returns.

That percentage holds for the 2000’s as well, with 17 of 22 years showing positive returns (2000 – 2021).

GPD

MANUFACTURING

The capacity utilization rate stayed above 75 for the entire year. This signals that factories, while busy, have the capacity to increase production should demand rise.

Inventory to sales ratios confirm the effects of the pandemic. Retail inventories to sales ratios are 22% below their 10-year averages, indicating strong sales and low inventory supply, while manufacturing inventories are above their 10-year averages as manufacturers are pre-buying raw materials due to delivery timing issues. Wholesale inventories are at their 10-year averages.

EMPLOYMENT

One way to analyze the employment situation is to look at the raw data. There are 261 million people in the U.S. of working age. Of those, 161 million are “wanting to work”. Of those 161 million persons wanting to work, 152 million are currently employed, leaving 9 million unemployed. Another way to look at the data is that there are 100 million people of working age who do not “want to work” – highest in history - (age, in school, stay at home parent, etc.) plus another 9 million people who want to work but are not employed.

Looking over the past 5 years (2017 – 2021) the U.S. added 6.4 million people of working age, 5.4 million who do not “want to work”, thus adding only 1 million people to the eligible labor force. The number of unemployed has increased by 1.7 million, resulting in 700,000 less people working in 2021 than were working in 2017!

We can also look at the data to view the percentage of individuals wanting to work with the percentage actually employed. Currently, 61.7% of the U.S. population wants to work (down from 66% 10 years ago) and 58.4% are working. The big question is whether this downward trend will continue post pandemic.

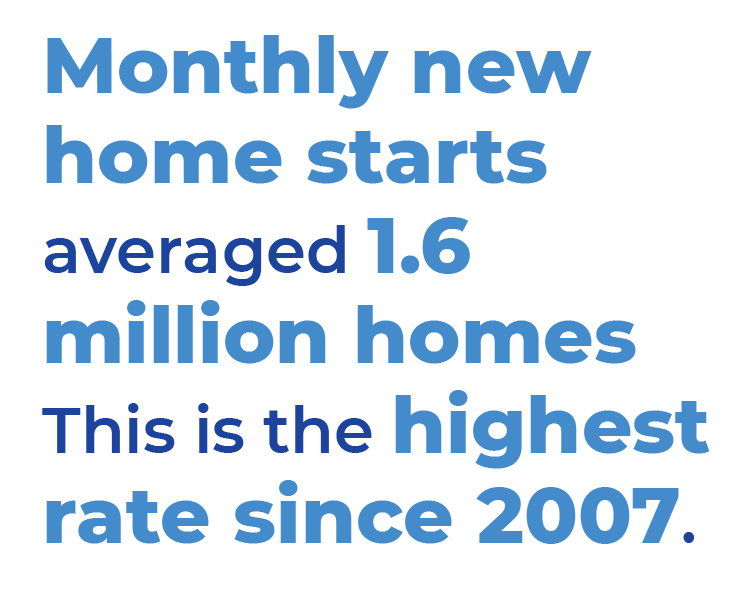

HOUSING

Sales of existing homes followed the same pattern, dropping significantly during the shutdown, but rebounded to end the year on a 6.7 million per year pace due to the pent-up demand.

The interest rate on a 30-year fixed rate mortgage continued to promote home sales. Rates started the year at 2.67% and finished the year at 3.11%. These rates are low by historical standards.

HOUSING

CONSUMER SENTIMENT

CONSUMER SALES

Sales of new vehicles took a big hit during the year as supply issues left most dealership lots without vehicles to sell. New vehicle sales dropped to an annualized pace of 13 million vehicles during the end of the year down from an annual pace of 17 million in January.

INTEREST RATES

INFLATION

OIL

US DOLLAR

STOCKS

The above rise in corporate profits caused the S&P 500 Price to Earnings (PE) ratio to drop from 31 to 22 during the year. That puts current valuations back in line with both the long-term 10-year and 20-year averages.

BONDS

RECAP

Jerry VanderLugt CPA, CFP, CVA

Matthew Kunnen, CFA, CFP

Chad Soukup, CPA, CFP

REFERENCES:

Related posts

{kind=link}

{kind=link}

{kind=link}

August 20, 2025